How Marketplaces Can Monetise Payments: Turning Every Transaction into Profit

Most marketplaces treat payments as a cost centre. Here’s how to turn every transaction into profit through embedded payments and smarter monetisation models.

The problem with seeing payments as just “plumbing”

Not long ago, I was chatting with a founder of a fast-scaling marketplace in Southeast Asia.

Their platform had processed over $20 million in transactions that year.

When I asked, “How much revenue did you make from payments?”

They said, “None — it all goes through Stripe.”

That’s the reality for most marketplaces today.

Payments are treated like a back-office function — a cost of doing business — rather than a profit opportunity.

But here’s the thing:

If your platform moves money, you’re already sitting on a hidden revenue stream.

You just haven’t monetised it yet.

Marketplaces are becoming financial ecosystems

Over the past few years, the definition of a marketplace has evolved.

They’re no longer just matching supply and demand — they’re orchestrating commerce, payments, and trust across multi-party networks.

And as marketplaces scale, one function underpins everything: payments.

Payments affect:

- How fast suppliers or freelancers get paid

- How customers perceive trust and reliability

- How much liquidity flows through the ecosystem

In short: payments aren’t backend anymore — they’re strategic.

Yet, most marketplaces outsource them entirely to third parties (like Stripe or PayPal) and miss the chance to turn them into a profit engine.

The Missed Opportunity: Payments are your most frequent touchpoint

Think about it.

Every gig, every project, every delivery — every single one involves a payment.

And each payment is a moment to:

- Add value

- Capture margin

- Deepen loyalty

But when you rely on third-party processors, all that value leaks out.

Your platform becomes just a pass-through layer, losing out on:

- Transaction margins

- Float income

- Interchange revenue

- FX spreads

- Embedded lending or early pay fees

It’s like owning a toll road but letting someone else collect the tolls.

The Solution: Turn payments into a profit centre

So how do you monetise payments without becoming a bank?

The answer: embedded payments infrastructure.

By embedding payment capabilities directly into your marketplace — through partners like MyGigsters — you can control how funds flow between your buyers and sellers, and monetise every step of that flow.

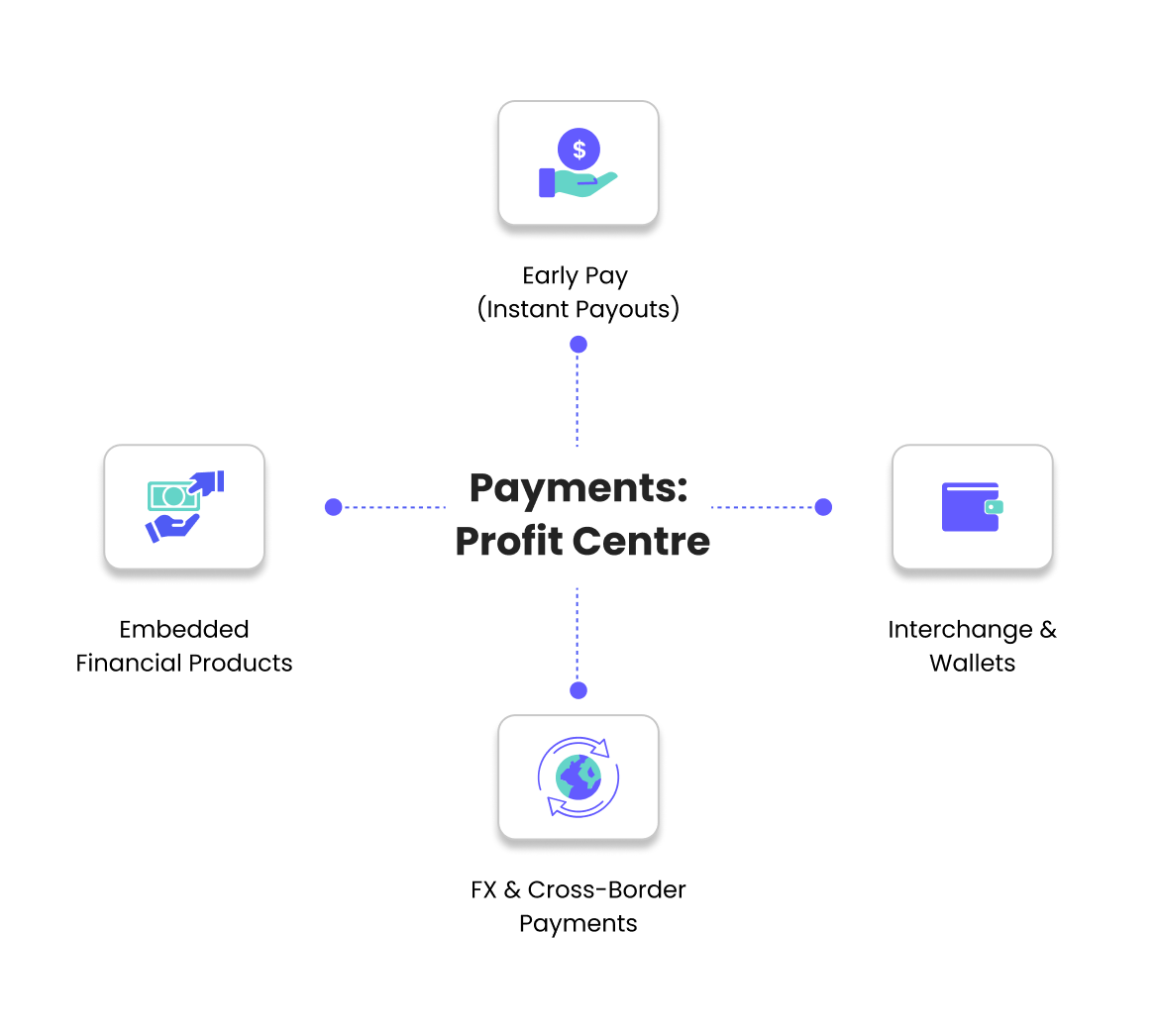

1. Early Pay (Instant Payouts) — the easiest revenue lever

Let’s start with the simplest model:

Offer faster payouts for a small fee.

Example:

- A freelancer completes a $500 project.

- You offer “Instant Pay” for a 2% fee ($10).

- Even if only 15% of users opt in, that’s a 3–5x uplift in transaction revenue.

This works because you’re solving a real pain: cash flow.

And people are happy to pay for speed when it helps them manage their week better.

That’s exactly what leading gig platforms do — monetising urgency while improving loyalty.

2. Interchange & Wallets — every swipe can earn

If your platform enables users to spend via an in-app wallet or branded card, you can earn a share of interchange revenue — the small percentage paid by merchants on each transaction.

Imagine:

- A driver’s wallet receives $1,000 in weekly earnings.

- They spend half using your card.

- Each transaction generates interchange — revenue that compounds at scale.

This is why wallets are the new goldmine.

They don’t just improve experience — they build new income streams on everyday spending.

3. FX & Cross-Border Payments — own the spread

If your marketplace operates internationally, there’s a hidden margin in foreign exchange (FX).

Instead of passing that spread to your payment processor, you can capture a portion through embedded global wallets or multi-currency settlements.

Example:

- Platform handles USD-INR or AUD-IDR transfers.

- By using embedded wallets, you control when and how conversions happen.

- Each transaction can generate 0.5–1% margin — pure revenue.

This is particularly powerful for remote talent marketplaces or cross-border logistics.

4. Split Payments & Fee Optimisation

Every marketplace deals with multi-party payouts — splitting payments between suppliers, contractors, and commissions.

By embedding your own payment logic, you can:

- Automate fee deductions

- Optimise transaction routing (reduce gateway costs)

- Introduce premium fee tiers (e.g., “Express Payout,” “Verified Partner”)

This not only saves time and admin cost but creates premium monetisation tiers that users willingly pay for.

5. Embedded Financial Products — your ecosystem, your upsell

Once your payment infrastructure is embedded, it becomes the foundation for other revenue-generating financial services:

- Microloans for top-performing users (funded by lending partners)

- Insurance for gig workers or service providers

- Savings and tax tools embedded within wallets

Each of these can generate revenue through referral or commission models — while improving worker financial health and retention.

That’s the magic of embedded finance:

It aligns your profit with your users’ wellbeing.

The Numbers: How much can you actually earn?

Here’s a quick breakdown based on typical marketplace volumes:

Even at modest adoption rates, this adds 6–10% incremental margin to your existing GMV — without raising prices.

Case Example: A marketplace that flipped the script

A logistics platform using MyGigsters’ Orbit Suite introduced early pay and wallet-based payouts for their driver network.

In six months:

- 18% of drivers opted for instant pay (2% fee)

- Platform generated 4.2x uplift in revenue per transaction

- Active driver retention increased by 37%

That’s the power of owning your payment rails.

The Founder’s Takeaway: Payments are your profit moat

Most founders still see payments as a technical checkbox:

“Does it work? Great, move on.”

But the best operators see it as a growth lever — the foundation for retention, data insights, and revenue expansion.

When you control your financial infrastructure, you control your margins, speed, and loyalty loop.

Embedded payments don’t just process transactions — they compound your economics.

Final Thought

If you’re a marketplace founder, you don’t need to build a bank.

You just need to stop giving your bank away.

Every dollar that moves through your platform is a moment of trust — and an opportunity for value creation.

Don’t let that value leak.

Own it, embed it, and monetise it.