Embedded Payments for Marketplaces: How Platforms Can Scale Globally Without Banking Licenses

Embedded Payments: The Gateway to Global Marketplace Expansion

As marketplaces expand across borders, the ability to facilitate payments—and payouts—efficiently becomes pivotal. But acquiring banking licenses globally? That’s resource-intensive, complex, and often impractical. Enter embedded payments: the secret sauce allowing platforms to scale internationally without turning into banks.

What Are Embedded Payments?

Embedded payments allow platforms to offer payment acceptance and seamless payouts directly inside their own ecosystem. Instead of redirecting to banks or external payment gateways, marketplaces can: (World Economic Forum).

- Accept card, wallet, or bank payments at checkout.

- Orchestrate payouts to freelancers, drivers, and sellers instantly.

- Manage FX and cross-border transactions without owning a banking license.

At MyGigsters, we built this as-a-service layer: platforms plug into our APIs and orchestration engine, and we handle everything from onboarding & KYC to settlement and global currency wallets.

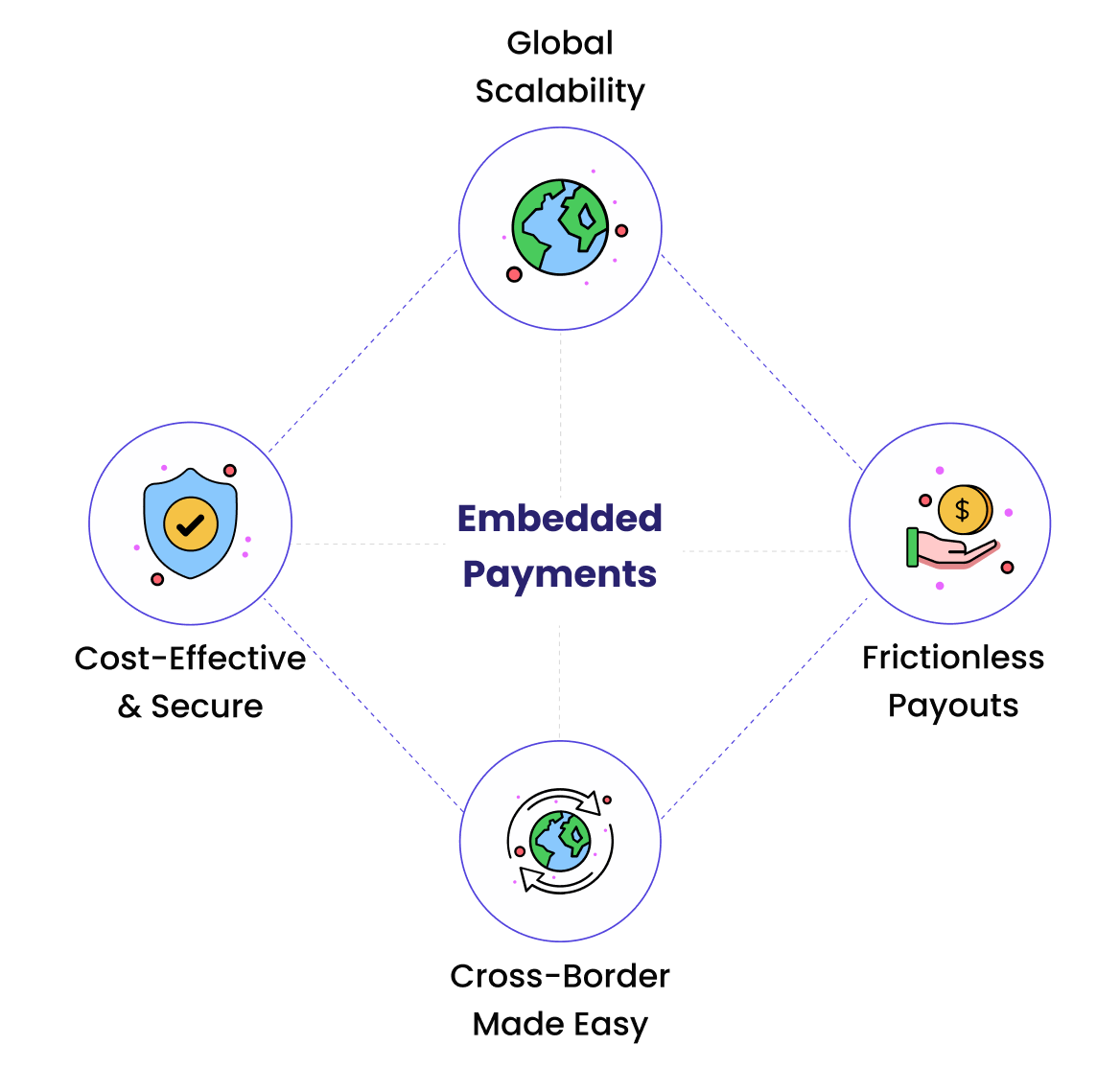

Why Marketplaces Love Embedded Payments

- Global Scalability Without Licensing Headaches

Platforms like MyGigsters enable marketplaces to operate in 135+ currencies, all through a streamlined single integration. No need for localized banking setups or multiple licensing regimes. - Frictionless Payouts Drive Loyalty

Embedded payouts are increasingly critical for retaining sellers or creators. Yet, payouts remain less mature than payment acceptance (Flagship Advisory Partners).

With MyGigsters Early Pay, marketplaces can increase per-transaction revenue while giving independent workers access to funds instantly—without holding payout risk themselves. - Cross-Border Made Easy

Traditional correspondent banking networks are often slow and opaque. Embedded platforms can bypass that with local payment rails, dynamic FX, and even blockchain-enabled transfers for faster, cheaper, and transparent cross-border flows (EY, Macro Global, WhiteSight, B2e Media Ltd.). - Cost-Effective & Secure

Embedded finance often brings competitive FX rates, transparent fees, and streamlined compliance—all baked into the user experience (Macro Global, B2e Media Ltd.).

How Embedded Payments Work Without Banking Licenses

1. Partnering with Licensed Fintech Providers

Platforms tap into fintechs like MyGigsters, Stripe, Adyen, or Mangopay—already licensed across jurisdictions—to handle payments. These providers shoulder regulatory burdens, while platforms remain focused on their core product.

- MyGigsters Embedded Finance Rails: Platform-first and API-driven rails that handles everything from payment orchestration to compliance and instant payouts.

- Stripe Connect: Single integration, multi-currency payout infrastructure, and compliance built-in(Stripe).

- Adyen: Functions as an acquirer across markets with its own licences and risk tools(Adyen).

- Mangopay: An EU-licensed payments infrastructure used by marketplaces like Vinted and Rakuten, also supporting FX and local payouts.

2. Using Embedded Finance APIs

Providers such as MyGigsters provide turnkey APIs for everything from payout splits to managing local currencies—enabling rapid market entry without building from scratch.

3. Compliance & Regulation via Fintech Network

Rather than securing local money-transmitter or payment institution licenses, marketplaces operate under the umbrella of their fintech partners. The fintech handles KYC/AML, cross-border regulation, and settlement, reducing friction and risk for the marketplace itself.

Marketplace Advantage: Real-World Benefits

Looking Ahead: Embedded Payments in 2025+

- Massive Market Growth: The global embedded payments market reached $24.7 billion in 2024 and is projected to grow at a 30.3% CAGR to $333.7 billion by 2034 (Global Market Insights Inc.).

- Cross-Border Innovation: Blockchain, tokenization, and central bank digital currencies are militarizing real-time, borderless rails—potential disruptors to traditional SWIFT systems (Financial Times, Investors).

- Use Case Evolution: From creator payouts to B2B invoicing, embedded finance use cases are exploding (WIRED, Macro Global).

Final Thoughts

Embedded payments empower marketplaces to scale globally without morass of banking licenses. By partnering with licensed fintechs, integrating robust APIs, and leveraging embedded finance rails, platforms can offer seamless payments and payouts—locally and globally—at scale. This isn't the future. It's happening now.

Marketplaces thrive when payments disappear into the background. MyGigsters makes that possible.

We’re not just a payments provider—we’re a platform-first financial infrastructure that enables growth, retention, and compliance across borders.

👉 Discover how MyGigsters can power your embedded payments and payouts.

References

- Embedded finance market context and trends (Payby, World Economic Forum, WIRED)

- Stripe Connect global scalability benefits (Stripe)

- Embedded payouts growth opportunities (Flagship Advisory Partners)

- Rapyd’s payout infrastructure details (Rapyd)

- Cross-border payments inefficiencies and embedded solutions (EY, Macro Global, WhiteSight, B2e Media Ltd.)

- Adyen embedded payments and licensing (Adyen, Wikipedia)

- Mangopay marketplace infrastructure and FX (Wikipedia)

- Embedded payments industry size and growth projections (Global Market Insights Inc.)

- Emerging cross-border payment technologies (Financial Times, Investors)