Beyond Payments: How Embedded Finance Drives Marketplace Retention and Revenue Growth

Embedded finance isn’t just about payments — it’s how modern marketplaces boost retention, trust, and revenue growth while deepening loyalty with every transaction.

Why retention is the new growth

A few months ago, I caught up with a founder running a fast-growing freelance marketplace.

They were adding thousands of new users every month, but there was one painful metric they couldn’t ignore — churn.

Despite the influx of signups, 40% of freelancers stopped using the platform after just three jobs.

Sound familiar?

It’s the silent killer in the marketplace world — leaky retention. You can pour all your dollars into acquisition, but if your users aren’t staying, you’re burning fuel with no lift.

That’s when the founder realised:

“Our platform doesn’t just need faster payments; it needs embedded finance that makes freelancers feel like insiders, not outsiders.”

Marketplaces are more than matchmakers

Let’s be honest — most marketplaces start the same way. You connect supply and demand, take a small fee, and focus on growth.

But as competition heats up, the ones that win are those who evolve beyond being a “matchmaker.”

They become financial enablers — helping their users earn, manage, and grow money within the ecosystem itself.

That’s what embedded finance is all about.

It’s not a buzzword. It’s a strategy that transforms platforms from being transactional to relational.

From being “just another app” to becoming an essential part of a worker’s livelihood.

What exactly is Embedded Finance (and why it matters for platforms)

At its simplest, embedded finance means integrating financial services — like payments, wallets, lending, insurance, and savings — directly into your platform.

Think of it like this: instead of sending users to banks or third-party providers, you become the bank (without actually becoming one).

Examples of embedded finance in action:

- Instant Payouts (Early Pay): Workers access their earnings immediately after completing a task.

- Split Payments: Revenue automatically divided among contractors, suppliers, or partners.

- Wallets & Cards: In-platform wallets or debit cards for everyday spending.

- Microcredit: Small working capital loans for gig workers or sellers to scale.

- Insurance & Super: On-demand protection or retirement savings for independent workers.

Each of these features deepens engagement. Why? Because money is emotional. Once users trust you with their money, they stay longer, transact more, and advocate for you.

The Big Shift: From transactions to trust

Here’s the truth every marketplace founder eventually learns — retention is built on trust, not incentives.

And nothing builds trust faster than reliable, transparent, and instant financial experiences.

When a driver gets paid instantly after a shift,

When a freelancer doesn’t need to chase invoices,

When a delivery partner can see their earnings in real time —

That’s when loyalty is built.

We’ve seen this firsthand at MyGigsters, working with marketplaces across delivery, on-demand talent, and logistics.

Platforms offering embedded payouts and early pay options report up to:

- 30–50% increase in repeat transactions

- 40% lower churn among active workers

- 3–5x uplift in per-transaction revenue from monetised payment flows

That’s not just fintech magic — it’s user psychology.

The Retention Flywheel: Why embedded finance keeps users coming back

Here’s a simple framework — think of embedded finance as a retention flywheel:

Each layer compounds the next.

When users get paid easily, they trust you.

When they see value in staying, they engage more.

When you solve their financial pain points, they advocate for you.

That’s how embedded finance shifts marketplaces from being tools to trusted ecosystems.

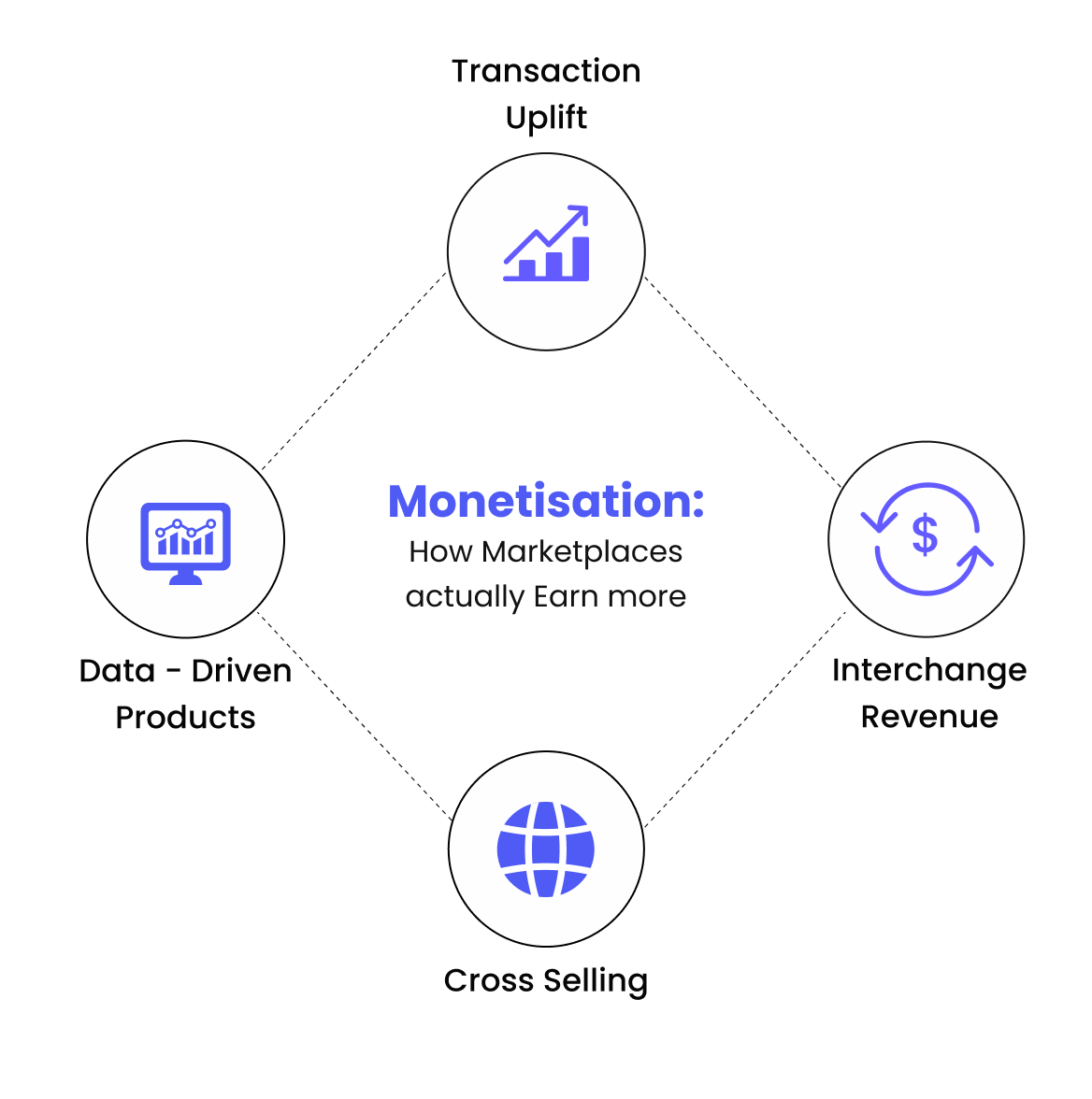

Monetisation: How marketplaces actually earn more

Let’s talk money — because embedded finance isn’t just a retention play. It’s a profitability engine.

Marketplaces using embedded finance can unlock new revenue streams without raising prices or commissions.

Here’s how:

1. Transaction Uplift (Early Pay Fees)

Workers opting for early payouts typically pay a small fee (1–3%).

Even if 10–20% of workers use it, that can 3–5x your per-transaction margin.

2. Interchange Revenue (Cards & Wallets)

When you issue branded debit cards or wallets, every transaction generates interchange fees — turning every swipe into revenue.

3. Cross-Selling (Insurance, Tax, Loans)

Offering micro-insurance or instant credit products via partners can drive referral fees, while improving user retention and trust.

4. Float & FX Margins

Managing multi-currency transactions or holding wallet balances creates small but scalable margin opportunities.

5. Data-Driven Products

By owning transaction data, platforms can offer predictive services — “cash flow projections,” “tax ready summaries,” etc.

It’s value creation on autopilot.

In short:

Embedded finance helps marketplaces earn from every transaction, not just take a commission from the match.

Case in Point: The ‘Platform Stickiness’ Effect

A delivery marketplace we worked with in India introduced early pay for 20% of their drivers.

Within 3 months:

- Active driver churn dropped by 45%.

- Average monthly transactions per driver increased by 38%.

- Platform revenue grew 4x from monetised payouts.

That’s what we call sticky growth — when your users are not just staying but earning more through you.

The Founder’s Lens: What this means for you

If you’re building or scaling a marketplace today, embedded finance is no longer optional.

It’s your competitive edge.

Here’s why founders are doubling down:

- It reduces dependency on external payment systems like Stripe (which weren’t built for multi-party flows).

- It builds loyalty through transparent, fast, and localised payouts.

- It creates margin leverage — you grow revenue per transaction without raising fees.

- And most importantly, it turns your marketplace into a financial hub, not just a matching engine.

The future of marketplaces belongs to those who can offer value beyond the job — where every transaction strengthens the relationship.

The Takeaway

Embedded finance isn’t just about making payments easier.

It’s about making your platform indispensable.

When you help your users earn faster, manage smarter, and save better — you’re not just another app on their phone.

You become their financial ally.

And that’s how marketplaces grow — not through acquisition, but through trust, retention, and monetisation that compounds over time.

Final Thought

The next wave of marketplace innovation won’t come from better matching algorithms.

It’ll come from financial experiences that build loyalty.

If your platform isn’t embedding finance yet, you’re not just leaving money on the table — you’re leaving trust behind.

👉 Discover how MyGigsters helps marketplaces embed payments, automate payouts, and unlock new revenue streams through early pay and financial services.