Financial Tools as Competitive Moat: How Smart Platforms Cut Gig Worker Churn by 47% Through Embedded Finance

Financial Tools as Competitive Moat: How Smart Platforms Cut Gig Worker Churn by 47% Through Embedded Finance

The most expensive mistake gig platforms make? Treating payments like a utility instead of a retention weapon.

I've watched 50+ marketplaces burn through millions acquiring gig workers, only to lose them to competitors offering marginally better payment terms. The brutal truth: 73% of gig workers will switch platforms for faster payments, and 68% cite financial stress as their primary reason for reducing platform activity.

But here's what most platform builders miss—the winners aren't just processing payments faster. They're using embedded financial tools to create switching costs that keep workers locked in long after the initial novelty wears off.

The Hidden Cost of Gig Worker Churn

Before diving into solutions, let's quantify the problem. Industry data from 2025 shows:

- Average gig worker acquisition cost: $127-$340 per worker (varies by sector)

- Median gig worker lifetime value: $2,400-$8,900 depending on engagement

- Annual churn rates: 68% for food delivery, 51% for ride-share, 43% for service marketplaces

The math is sobering. If you're acquiring workers at $200 each and losing 60% within the first year, you need each retained worker to generate $500+ just to break even on acquisition costs.

Real Example: A regional delivery platform I consulted for was spending $2.1M annually acquiring drivers, with 71% churning within 8 months. Their customer acquisition payback period? 18 months. They were hemorrhaging cash.

Why Traditional Retention Strategies Fail

Most platforms approach gig worker retention like they're running a SaaS business:

- Gamification and badges

- Promotional bonuses

- Referral programs

- Better customer support

These help, but they miss the core issue: gig workers are financially stressed, and traditional retention tools don't address their fundamental money problems.

According to Earnin's 2025 Financial Health Report:

- 78% of gig workers experience cash flow gaps between jobs

- 64% have used payday loans or overdraft fees in the past year

- 41% would work more hours if paid instantly instead of waiting 2-7 days

The opportunity is obvious: solve their financial stress, and they'll stick around.

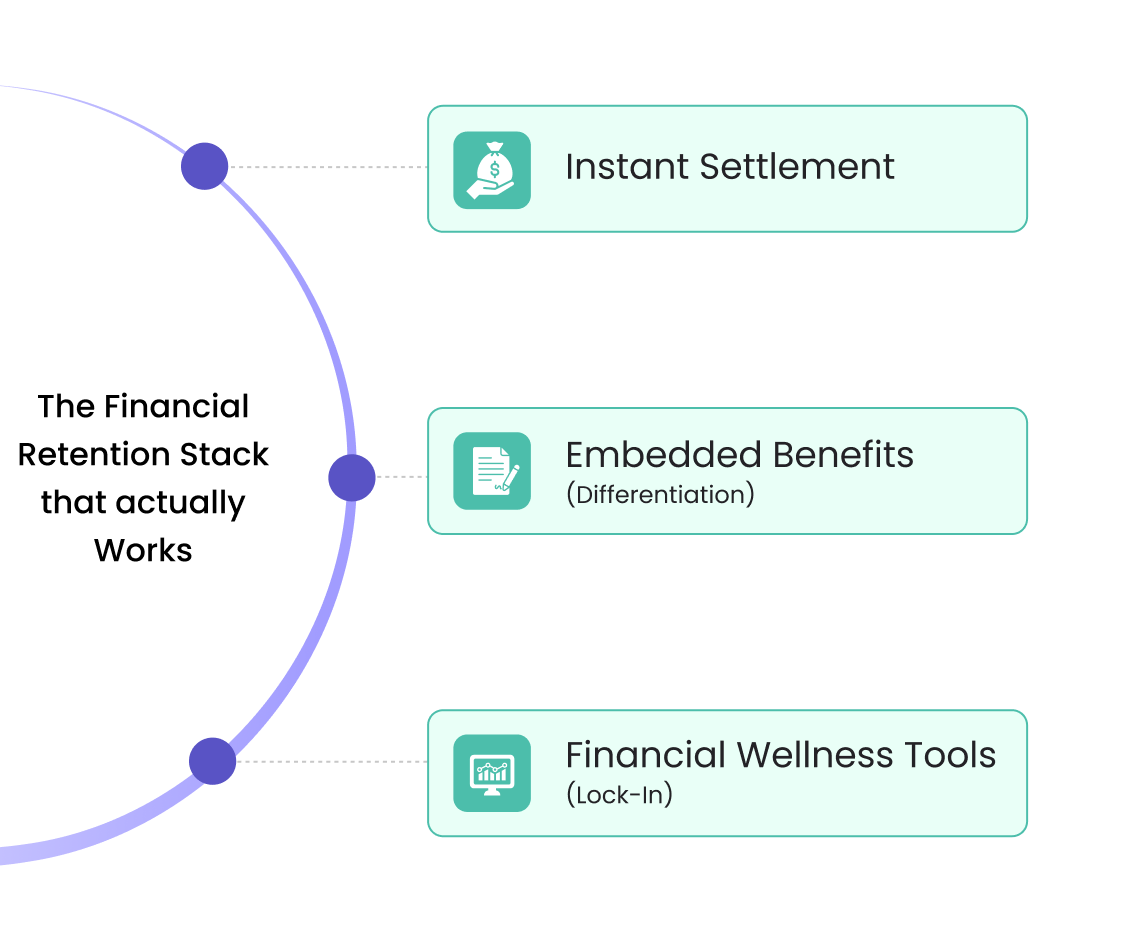

The Financial Retention Stack That Actually Works

After analyzing the most successful gig platforms (those with <30% annual churn), a clear pattern emerges. They don't just process payments—they provide a financial wellness stack that creates genuine stickiness.

Layer 1: Instant Settlement (Foundation)

What it is: Real-time payment processing with instant cashout options.

Why it works: Removes the cash flow gap that drives workers to juggle multiple platforms. When workers can access earnings immediately after completing a job, they consolidate their activity on platforms that offer this convenience.

Implementation reality: True instant settlement requires significant infrastructure investment. You need payment rails that bypass traditional ACH delays, sufficient capital for pre-funding, and sophisticated risk management to prevent fraud.

The numbers: Platforms offering instant pay see 32% higher worker retention in months 6-12 compared to those with standard 2-7 day settlement cycles.

Layer 2: Embedded Benefits (Differentiation)

What it is: Native insurance, super contributions, tax optimization tools built directly into the platform experience.

Why it works: Eliminates the administrative burden that drives gig workers away from independent work. When benefits are automatic and embedded, workers don't need to manage multiple vendor relationships.

Competitive moat: This creates significant switching costs. A driver who's built up 6 months of tax records and insurance coverage through your platform won't easily migrate to a competitor.

Real example: A healthcare platform I worked with integrated automatic insurance verification and claim processing. Their practitioner retention improved by 43% year-over-year, and average revenue per practitioner increased 28% as workers took on more jobs within the ecosystem.

Layer 3: Financial Wellness Tools (Lock-in)

What it is: Spending insights, savings automation, credit building, early wage access for regular workers.

Why it works: Creates daily engagement beyond job completion. Workers interact with your platform for financial management, not just work coordination.

The data: Platforms with embedded financial wellness see 2.3x higher daily active usage and 51% longer average worker tenure.

Case Study: How One Platform Cut Churn 47% in 8 Months

Background: Regional service marketplace with 12,000 active contractors, 62% annual churn, struggling to scale beyond $8M GMV.

The Problem: Workers constantly compared the platform against national competitors. Price competition was impossible—the big players could afford to subsidize jobs. The platform needed non-price differentiation.

The Solution (MyGigsters Implementation):

- Instant Settlement: Implemented same-day payment processing for all completed jobs

- Embedded Tax Tools: Automated ABN verification, expense tracking, and quarterly BAS preparation

- Benefits Integration: Partner agreements for discounted insurance and super optimization

- Financial Dashboard: Real-time earnings analytics, goal setting, and cash flow projections

Results After 8 Months:

- Annual churn dropped from 62% to 33% (47% improvement)

- Average worker revenue increased 34% (workers took more jobs within ecosystem)

- GMV grew from $8M to $13.2M without increasing acquisition spend

- Worker NPS increased from 23 to 67

Key insight: The retention improvement wasn't just about the tools—it was about positioning the platform as a financial partner rather than just a job coordinator.

Implementation Framework: Building Your Financial Retention Stack

Based on patterns from successful implementations, here's the priority order for platform builders:

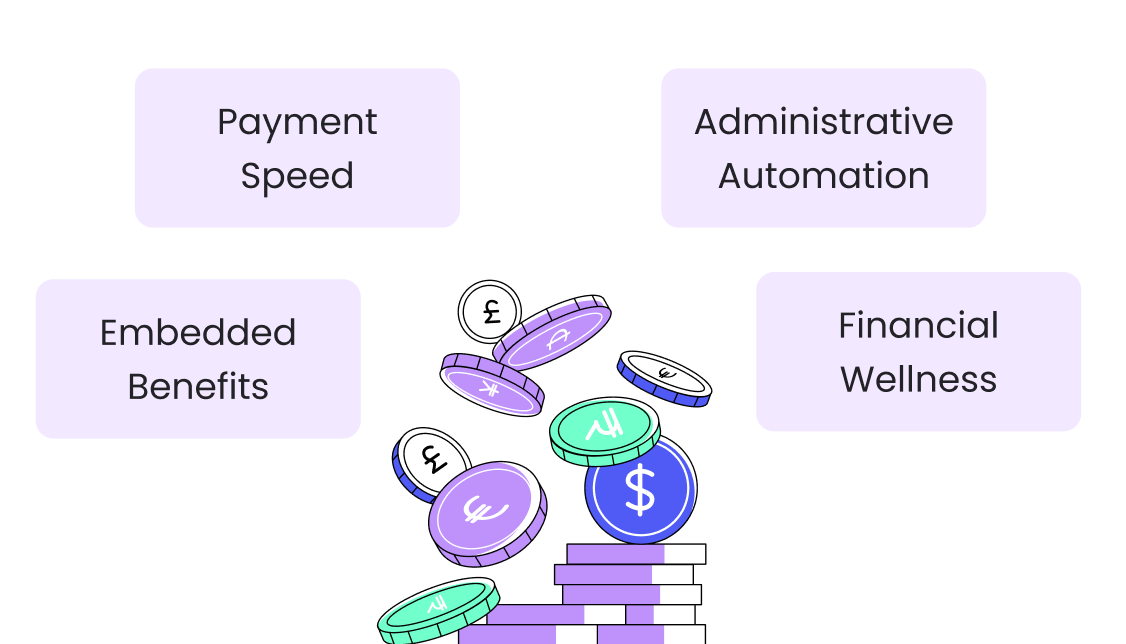

Phase 1: Payment Speed (Weeks 1-6)

- Implement instant settlement for completed jobs

- Add transparent fee structure (no hidden costs)

- Provide payment status visibility and notifications

ROI Timeline: 4-6 weeks to see retention impact

Investment Required: Medium (payment infrastructure + capital requirements)

Phase 2: Administrative Automation (Weeks 6-12)

- Automate tax document generation (1099s, expense tracking)

- Integrate compliance verification (ABN checks, right-to-work, insurance)

- Add earnings analytics and reporting tools

ROI Timeline: 8-10 weeks (longer-term retention impact)

Investment Required: Low-Medium (mostly API integrations)

Phase 3: Embedded Benefits (Months 3-6)

- Partner with insurance providers for group coverage

- Add superannuation contribution automation

- Implement credit building programs

ROI Timeline: 12-16 weeks (highest switching cost creation)

Investment Required: High (partnership agreements + compliance overhead)

Phase 4: Financial Wellness (Months 6+)

- Advanced analytics and goal-setting tools

- Savings automation and cash flow management

- Early wage access for regular contracted workers

ROI Timeline: 16+ weeks (deepest engagement and lock-in)

Investment Required: High (sophisticated financial product development)

The Competitive Reality: Why Most Platforms Don't Do This

If financial tools are so effective for retention, why isn't every platform implementing them? Three main barriers:

1. Capital Requirements

Instant settlement requires pre-funding worker payments before platform receives customer payments. For a platform processing $10M monthly GMV, this might require $2-4M in working capital.

2. Regulatory Complexity

Embedded financial services trigger compliance requirements. Depending on jurisdiction, you might need payment services licensing, credit licensing, or insurance distribution permits.

3. Technical Complexity

Building financial tools requires different expertise than building marketplace software. Payment orchestration, risk management, and financial product development are specialized skills.

The opportunity: These barriers create a moat for platforms willing to invest in embedded finance. Once implemented, competitors face significant catch-up costs.

ROI Analysis: Justifying the Investment

Conservative ROI Model (12-month horizon):

- Baseline churn rate: 55%

- Improved churn rate: 35% (38% improvement)

- Average worker LTV: $3,200

- Implementation cost: $450,000 (for 5,000-worker platform)

Financial Impact:

- Workers retained annually: 1,000 additional

- Incremental revenue: $3.2M

- Net ROI: 612% (after implementation costs)

The math: Even with conservative estimates, financial retention tools typically pay for themselves within 6-8 months through reduced acquisition costs and increased worker productivity.

Common Implementation Mistakes to Avoid

1. Treating Financial Tools as Add-Ons

Wrong approach: Building financial features as separate products or partner integrations.

Right approach: Embedding financial capabilities directly into core worker workflows. Payment status should be visible in job completion screens, tax tools should auto-populate from job data.

2. Over-Complicating the User Experience

Wrong approach: Requiring workers to set up separate accounts or learn complex financial management interfaces.

Right approach: Financial tools should feel like natural extensions of existing platform interactions. Default settings should work for 80% of use cases.

3. Ignoring Regional Compliance

Wrong approach: Implementing US-focused solutions without considering local requirements.

Right approach: Build compliance-first. In Australia, this means ABN verification, superannuation requirements, and appropriate tax withholding for different worker classifications.

The Future: Financial Tools as Platform DNA

The most successful gig platforms of 2026 don't think of themselves as marketplaces with payment processing. They think of themselves as financial service providers that happen to coordinate work.

This shift isn't just about worker retention—it's about business model evolution:

- Revenue diversification: Financial services generate 15-30% margins vs. 3-8% for transaction processing

- Data advantages: Financial data provides deeper insights for matching algorithms and risk assessment

- Network effects: Workers with embedded financial relationships refer other workers more frequently

Key Takeaways

- Financial stress is the #1 driver of gig worker churn—addressing it creates sustainable competitive advantage

- Instant settlement is table stakes—but embedded benefits and financial wellness create the real switching costs

- Implementation requires significant upfront investment—but ROI typically exceeds 400% within 12 months

- Regional compliance is critical—build for local requirements from day one

- Think platform, not marketplace—position financial tools as core value, not auxiliary services

The gig economy platforms that survive the next wave of competition won't be those with the best matching algorithms or the lowest fees. They'll be the ones that solve their workers' fundamental financial challenges.

Your workers are already stressed about money. The question is whether you'll help them solve it—or watch them find someone who will.

Frequently Asked Questions

Q: How much capital is required to offer instant settlement?

A: Typically 15-25% of monthly GMV as working capital, plus payment processing reserves. A platform processing $5M monthly might need $1-1.5M in working capital.

Q: What financial licenses are required for embedded benefits?

A: Depends on services offered. Payment services licensing for settlement, potentially credit licensing for wage advances, insurance distribution permits for benefits. Consult local regulators.

Q: How quickly do financial tools impact worker retention?

A: Instant settlement shows impact in 4-6 weeks. Embedded benefits and financial wellness tools typically take 12-16 weeks to show full retention impact.

Q: Can small platforms compete with big players on financial tools?

A: Yes, through embedded finance partners. Platforms can offer sophisticated financial services without building everything in-house by integrating with specialized providers.

Q: What's the biggest risk in implementing financial retention tools?

A: Regulatory compliance failures. Financial services are heavily regulated, and violations can result in significant penalties or operational shutdowns. Invest in compliance expertise upfront.

Ready to turn financial tools into your competitive moat? Book a demo to see how MyGigsters' embedded finance platform can cut your worker churn while improving unit economics."